Of all watch designers Rolex is arguably the most famous and sort-after brand. Rolex make just under a million watches a year and each one benefits from incredible craftmanship and beautiful design. On top of that the resale market for Rolex watches is pretty solid.

None of this means you should buy one.

Fashion, Influence and Scarcity create a powerful concoction of emotional pressures driving you to purchase high value Time Pieces. Just because it feels right doesn’t mean it’s a good use of your capital. As you are responsible for your own financial health it is your job to figure out whether putchasing one is a good use of your money.

We are not disputing the value. A Rolex will always be a Rolex and the price will always be the price. Our concern is that for most people there are savvier financial moves they should be making instead of buying a Time Piece.

For most people the shrewdest financial move would be to NOT buy one.

Social Media - The Root of New Evil

One of the curious consequences of Social media is it drives attention towards extremes and makes them appear more mainstream than they are:

Extreme Opinions

Extreme Actions

Extreme Wealth

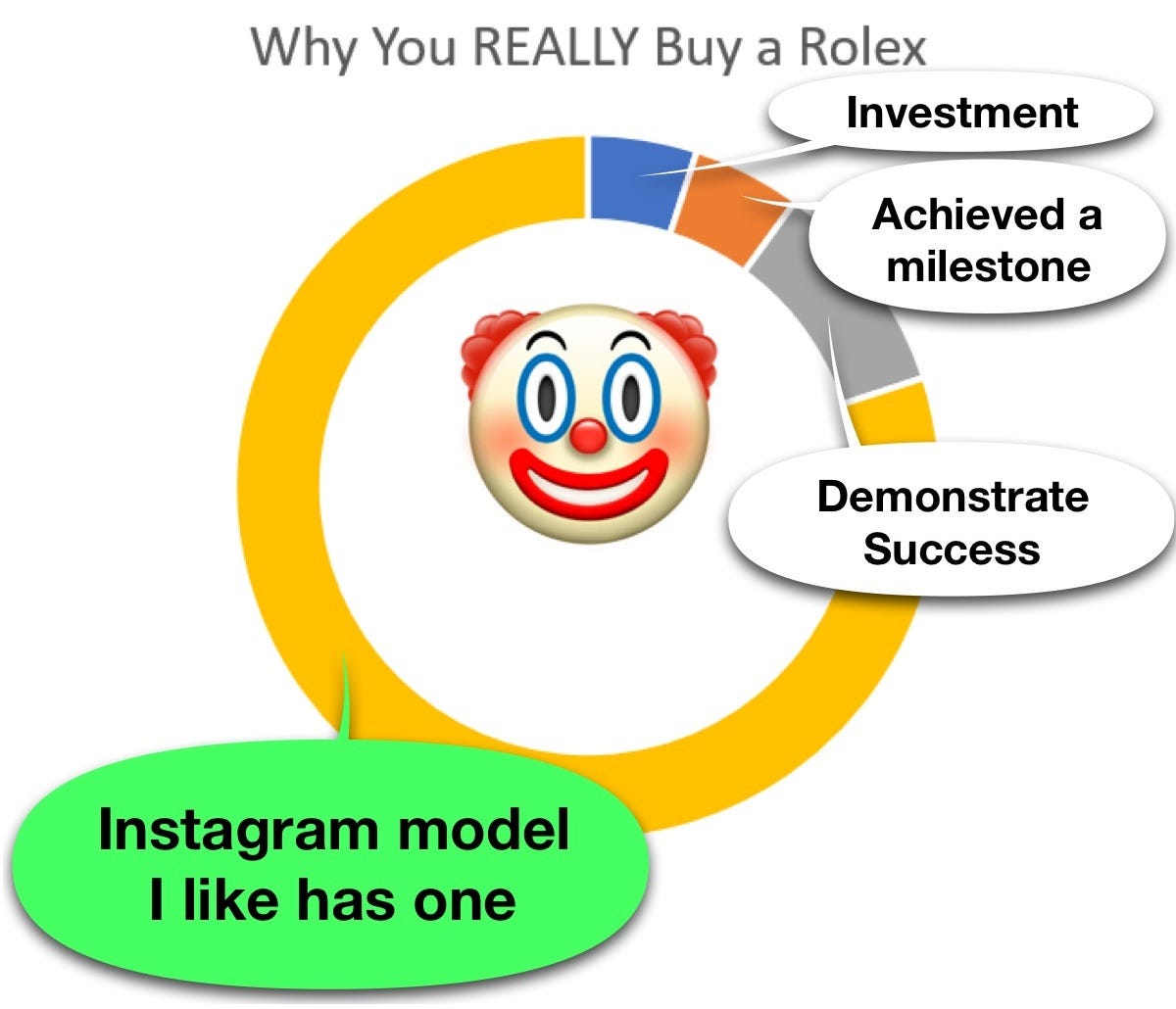

We are bombarded with images and stories from a tiny portion of the population who make a living from selling their ‘lifestyles’. Social media is a marketers wet dream.

‘Wealth Porn’ on social media has brought high value items to the mainstream attention in a way never seen before. Before social media you would see a Rolex on a handful of older wrists a month and almost without question under a suit peeking out from under the cuff. It was never being flaunted. Now you see them everywhere on increasingly younger wrists. Social media stars in their twenties flaunt Rolex’s and other collections online and the masses faun over them without understanding where the wealth has come from.

Social Media caused various fashion brands to break out towards elevated highs of Social Value. This isn’t a problem with products in the lower price brackets. Spending $200 on a t-shirt (that cost $1.50 to manufacture) is not the issue. For most this is a lavish spend on a t-shirt but shouldn’t affect their future or finances too much. You are unlikely going to take a line of credit to buy it (if you do then you need deeper help than we can offer here).

Why Are We Mad?

The problem comes when high ticket items become the rage and the “influence” generates social peer pressure to attain them. We are seeing this across a range of products like Cars, Bags, Watches and even destination holidays like Maldives or Yachts in Dubai.

Nobody Needs This Shit, They Want It!

The above products and services are potential fiscal killers to those who technically cannot afford them but strive to attain. You need (should aim to have) a substantial income and large capital reserves before you indulge in the finest material things the world has to offer. Without high income or retained wealth you have no choice but to lean on Credit (BAD) to secure these luxury items. Buying items you don’t need and can’t afford on credit is a dangerous pitfall for consumers but is wonderful for the economy.

Why? Example Time!

Step 1: See Watch you like on Instagram 🤩

Step 2: Find Watch online 💻

Step 3: Contemplate the price 😩

Step 4: Discover Financing Options 😎

Step 5: Buy Dream Watch on Finance 🥰

Step 6: Doom yourself to years of misery repaying it and crushing your plans to retire before you are 75. 😔

(Also apply this to Engagement Rings, Holidays & Cars you can’t afford).

Breakdown

The average income in the UK is £31,461 (2020). Below is the Rolex Yacht-Master Oyster, 44m with a retail price of £20,300 (oooo so pretty!)

The Doom Goblins in the Sales Department offer you the watch on Credit with an APR of 9.90% per annum. This is what you will pay….

In the end you have paid £26,822 for a watch that cost £20,300 (wow that interest stacks up quickly). This is financial equivalent of a coke and hooker’s weekend. You’ve spent a ton of money, had a wild 48 hrs and now can’t afford your rent or meds for your new range of venereal diseases.

Moral of the Story: Don’t use credit to buy expensive shit you don’t need and can’t afford.

Credit is fine for short term cash flow issues and long-term investment planning. It should never be used to buy stuff that loses value.

Till next time

The Wealth Gap