Watch out for this pension tax trap..

A UK focused article - This is NOT financial advice

Pensions are arguably the most generous tax wrapper we have in the UK. Unfortunately, that generosity only goes so far…

Pensions are amongst the most valuable (and boring) products available. If you have a substantial one you can retire comfortably, if you don’t… well there might be a way round that too.

Where do Pensions come from?

Back in the day pensions were paid for and provided by the company you worked for (or the government). Pensions were calculated based on your salary and your term of service. This meant you could work out decades in advance what income you might get from your pension in retirement. These are called ‘Defined Benefit’ pensions (DB for short).

DB pensions are great for pensioners as the responsibility for paying their pension falls on their old company. These days DB pensions are pretty awful for companies for the following reasons:

They are hugely expensive to run because pensioners are living much longer than they use to (how selfish of them).

A lot of these companies are struggling anyway as they are in industries that are on the decline.

DB Pensions became so burdensome for companies that many collapsed. Outside the public sector John Lewis might be the only company that still offers one. Most people currently working will have a less awesome (but still amazingly generous) Defined Contribution (DC for short).

With a DC pension you and you employer contribute monthly to your pension which is then invested in the markets. When you come to retire you have the following options:

Buy a guaranteed income for life from a private company

Take what you want from your pension pot when you want it

Do nothing!

Why are pensions awesome? (bare with us here…)

If you want to change the habits of a population you need a carrot and/or a stick. The government opted for a massive carrot shaped tax break for anyone with a pension. Here is how it works:

Paying into a pension

Payments made into a pension are made before tax. If you pay £80 from your wallet it gets boosted by 20% to £100 when it reaches your pension. Pension payments by your employer are paid before tax is calculated.

Tax within a pension

No Tax concerns (Boom)

Taking money out of your pension

25% can be taken tax free when you turn 55

the remaining 75% is taxed at your personal rate of income tax when you take it

When you die

Your pension is not included in the inheritance tax calculation. As inheritance tax is up to 40% that’s a BIG deal

If you die before you turn 75 your chosen beneficiaries can get have your pension tax free. If you die after age 75 they can draw from it but pay income tax on it based on their own personal rates.

Where does the pension generosity end?

There was no way the government was going to let us have infinite use of these tax breaks so Surprise Surprise they put some fairly substantial limitations on their generosity. These limitations are below:

Paying into a pension

You can’t contribute more than you earn (capped at £40k) and still receive the tax boost.

Taking money out of your pension (This is a Big One)

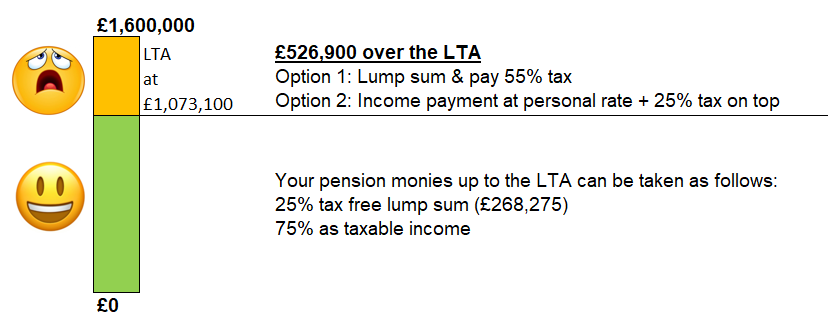

Once again the tax benefits are capped. You can take 25% tax free cash with the remaining 75% taxed as income tax up to the LIFETIME ALLOWANCE (LTA). Any pension monies you withdraw over the lifetime allowance (currently £1,073,100) suffer a hefty tax penalty…

HMRC will check whether you have gone over your LTA in several ways:

When you start taking money from a pension

When a DB pension in payment suddenly increases a lot

When you buy a guaranteed income for life using your pension

When you turn 75 with any sort of pension

A lot of people will get to their 75th birthday and receive a terrifying letter from HMRC asking them to prove how much of their LTA they have used. Nobody needs that kind of stress.

The good news is that any pensions in payment will have calculated how much of the LTA was used to pay your pension so if you have the paperwork it’s just a matter of adding up the percentages and reporting back to HMRC.

Some people will be lucky enough to have a protected lifetime allowance.

Summary

Looking at the tax breaks on offer you can see that the government is trying to get people to plan for their own retirements by offering great incentives. It didn’t work.

Even with these generous tax breaks people weren’t saving into pensions so the government forced employers to do it for them (Hello Auto Enrolment). Auto Enrolment has seen a massive take-up (no surprise when the government forces an entire population to save for their own future) and when they turn 55 these people will be glad that they have a nest egg to draw upon instead of being entirely dependent on the state pension.

If you are approaching retirement you really should speak to a financial adviser (not the same as an accountant). An adviser will help you plan for your financial future. It is always worth a conversation.

TheWealthGap View : The above content is a snapshot of the status quo. As already mentioned, there was a time when most people had a DB pension paid for by their company. As these companies failed, they were unable to provide pensions to their retired members. The government responded by setting up the Payment Protection Fund (PPF) which takes on the responsibility of providing pensions to pensioners of failed schemes. Click below to see how the PPF is funded

The point here is that since pension schemes have failed in the past its entirely possible that they will fail again in the future.

We believe that given the current Macro economic framework (zero interest rates and future debasement of currencies globally) it is pertinent for everyone to understand that a tax wrapper is only as effective as the investment within it. Historic trends on main stream equities and funds do not necessarily represent the future prospects of growth.

We feel it is important to point out to Millennials and younger generations that the next 50 years are unlikely to be like the last 50 (when have they ever!?). The transfer of wealth from the old analogue centralised banking systems into this new world of digital assets and tokenisation is already happening and CANNOT be ignored.

While still early and filled with extreme volatility we think everyone should still consider aiming to get some exposure into crypto assets (Please remember this is not financial advice). This asymmetric bet has the potential for monumental long term benefits if successful and offers an unparalleled seat at the table of the global wealth transfer happening through digitisation.

How can I get exposure in my pension to Bitcoin I hear you say?

We will cover this for our premium members. Join us via the link below to see how our co-founder turned his DC pension into a crypto exposed 600% gainer in 3 years.

Until next time

The Wealth Gap Team