You Work 5 Months A Year For Free! (Part 2)

In this follow up article we look at the options available to reduce your tax burden.

In part 1 we looked at how much tax the average British Citizen is paying (Scots pay more still). Its a lot more than most will realise. In this article we will look at the options available to you to reduce your tax burden and plan for the future.

Let’s look at what we can control:

Spending Habits

Pay More Into Your Pension & ISA

Invest for the future and use your Capital Gains allowance

Spending Habits

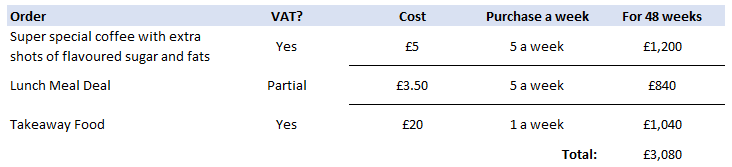

For The Love God make your own Coffee & Lunch

A coffee in the morning before work and a meal deal at lunch can easily cost you over £3,000 a year. Here is our spreadsheet:

The thing is, it’s never just a coffee either. It’s always a cookie as well. One day you might cave and buy a box of those delicious smelling chicken dipper things and before you know it your lunch meal deal is actually a starter for your 600-calorie pasta salad with a side box of chicken (I comfort eat).

Make your lunch. Brew your own coffee. Cut down on your VAT burden and invest your savings monthly.

Pay More Into Your Pension.

Pensions are arguably the most generous tax wrapper available in the U.K. and also the most tax efficient way of extracting money from a business. Let’s look at why:

That £80 in your pocket is worth £100 in your pension. It’s worth even more if you’re a higher rate tax payer as you can claim an additional 20% through you’re self-assessment. The government wants you to contribute to your pension which is why they add the tax you paid on your income back on your pension contributions.

There is no tax on any growth within your pension.

You can’t take any money from your pension until you are 55.

Once you are 55 you can take 25% of your pension as tax free cash (there is a cap to this generous feature called the Lifetime Allowance). Any further withdrawals are taxed against income tax.

You don’t have to pay inheritance tax on your pension when you die.

Pensions are supposed to encourage you to save for your future because most people cannot afford to live off the state pension alone. Pensions enjoy these generous tax breaks because the government doesn’t want to be on the hook for millions of pensioners who can’t afford to live.

Pay More Into your ISA

Coming a close second for tax efficient vehicles is the Investment Savings Account (ISA):

You can currently pay £20,000 a year into an ISA

Depending on who you go with you can invest in a large range of assets (from cash to stocks and shares)

There is no tax for you to pay on any gains within an ISA

Speculate to Accumulate

When we were young our elders told us to save money by putting it in the bank. They also told us to buy a house. In the past interest rates were over 5% and houses were a lot more affordable.

These days interest rates are 0.5% at best and property ownership has become increasingly unaffordable. We can no longer afford to build our lives around the advice given to us by our elders. Change is afoot and we need to be alert to the risks and opportunities it presents.

What Can You Do?

Everyone has options. Plan for the future, work out your personal income and expenditure. Talk to a financial adviser. Living in the present is a luxury few can afford. Everyone needs to save and invest for the future.

You Cannot Rely On The Government To Look After You

In September 2021 the UK government announced that National Insurance Contributions would increase. This followed the announcement that NHS workers would be getting a raise. This led to a quip by one nurse that she was paying for her own raise.

This is happening while the money printers are working away, adding more money to the economy which props up the markets whilst reducing the purchasing power of that same money. Everyone’s cash savings are being eroded daily by this practice 🤮.

Governments will continue to print money as it is easier politically to please people in the short term without forcing austerity. Politicians only think about the next Term of service and very few actually care about future outcomes. Popularity today is more important than affecting long term change.

Invest for the Future & Use your Capital Gains Tax Allowance

To build wealth for the future one needs to start purchasing assets that are likely to have future value, be that company shares, property or cryptocurrencies. Here at the Wealth Gap we strongly lean to the value of Network Effects and its entrance into Money markets with the invention of Bitcoin.

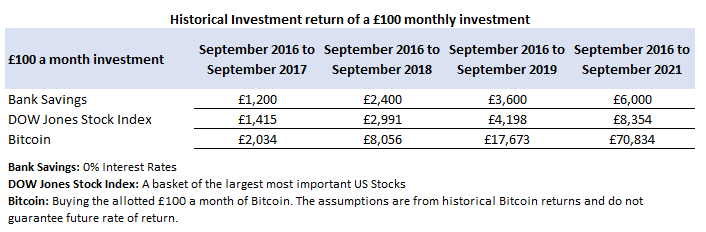

Let’s take a look what a £100 a month Bitcoin investment could have got you.

The chart speaks for itself. Bitcoin isn’t the only game in town but it is famous for its volatility and the riches it has brought to its early adopters. Regardless, the crypto industry is growing exponentially at present which means there could well be further opportunities for large gains.

This table is not a reflection of the future and change can occur to diminish returns but even with a factored in Risk of change you should be able to see that Cash is not going to save you or create future wealth.

The last 50 years will not be like the next 50 years in regards to finance and wealth building. The advice given and passed on by grandparents and parents alike was to save! This is a great practice of committing to taking action to improve one’s future by collecting value for later in life. The issue now is that currencies globally are being debased (Printed) at a phenomenal rate which is devaluing your future savings if its cash in the bank!

One must change with the times and act according to the potentials that are being presented.

What’s The Thing About Capital Gains?

If you have assets outside of an ISA you can use your capital gains allowance when you make a sale. Let’s use Bitcoin as an example:

Current Capital Gains allowance is £12,300

Capital Gains tax is 10% if you’re within your basic rate income tax band and 20% for anything over

Example: Joe Bloggs spent £100 a month on Bitcoin for 5 years spending £6,000 total. His Bitcoin is now worth £70,834, giving him taxable gain of £64,834. He can sell £12,300 of gains each year without having to pay any additional tax. For a £6,000 investment Joe has bought a tax free income of £12,300 for 5 and a bit years. Not bad eh?

No Risk No Reward

80% of the time markets go up yet we spend all of our emotional energies thinking about the 20% of the time they go down. Bitcoin is no different. Experience investing can help us grow comfortable with market volatility, as can long investment horizons.

In parting let us consider a few words of wisdom from the legendary billionaire investor Saruman The White, Lord of Isenguard

Until Next Time

The Wealth Gap