The Debt Markets Saga! Part 1/3

An easy introduction into the debt markets

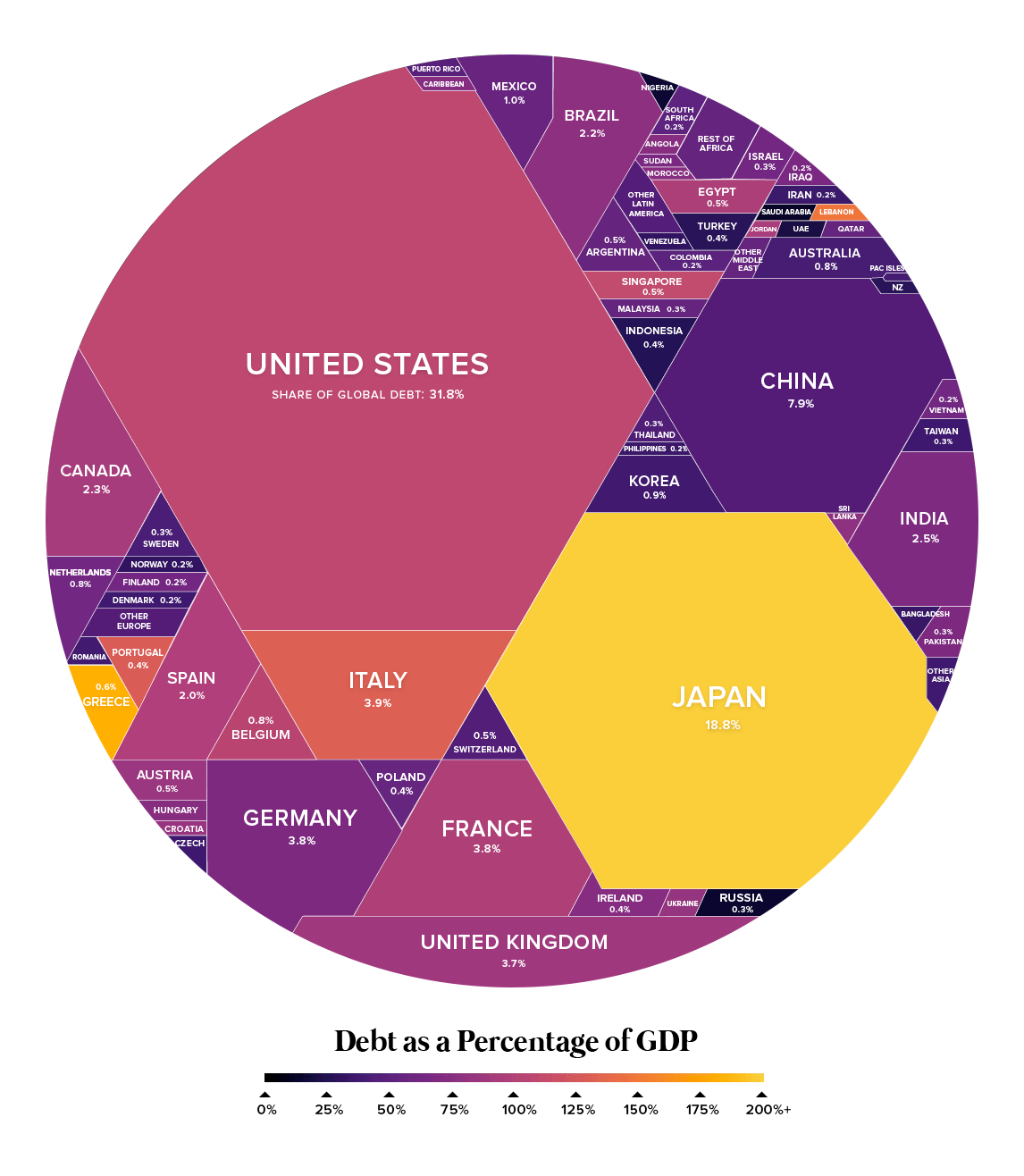

Lending money to nation states is BIG business. Its such big business that it is arguably the backbone of the whole financial system. Check out the bad boy below:

This picture is every countries debt to Gross Domestic Product. For example in Japan, every 100 Yuan created by the markets in a year carries over 200 Yuan of debt.

Buying Debt

We have recently read Gregg Foss’s ‘Why Every Fixed Income Investor Needs to Consider Bitcoin as Portfolio Insurance’ paper. We loved it and want to disseminate his knowledge into easy to follow, bitesize chunks for our readers. Unfortunately to understand his position we must first understand the Fixed Income Market. The remainder of this article will attempt to explain the fixed income markets in an interesting, easy to digest way 😊.

To do this we need some characters. Meet Ben…

Ben is a company (people are nicer to look at than logos). Ben can raise money in two ways:

Borrow money for a pre agreed amount (Fixed Income Instrument/Bond)

Selling the rights to his future profits (Shares)

How do Fixed Income Instruments (Bonds) Work?

Ben needs £100 and wants to pay it back in 5 years.

As Ben is such a steady guy lots of people are prepared to offer him the money. You agree to loan him £100 and Ben agrees to pay you £5 ever year for 5 years before finally returning the £100 (In 5 years you will get £125 back).

You & Ben sign a contract agreeing to the above. That’s it, you have just created a Fixed Income Instrument (Bond) Yay!

How do Shares Work?

Ben dazzles you with a brilliant invention that will change the world. He needs to raise some money to make it happen though. You and your friends are inspired by his vision and want to share in his success. You buy 1 share of Ben’s company for £1 (there are a 100) in the hope that Ben is a success and makes lots of money meaning you could sell your share for more than you bought it.

Food for thought:

If you hold a Bond with Ben and his company is massively successful you won’t benefit from the success (which sucks). All you get is your £100 + £25 back. If you hold Shares you benefit from the success and make money.

If Ben’s company takes a turn for the worse (the great idea disappoints) then your Shares will drop in value and your Bond is suddenly a lot riskier for the price you bought it for (making it harder to sell)

If Ben’s company goes bust the Bond gets dibs on the company’s assets, the Shares might be entitled to nothing.

The issue with Bonds is that your profit is capped at the very start while your potential losses are unlimited (this is called the downside risk) as Ben’s company could go into liquidation meaning you could lose all your money.

Lending Money to Governments:

Meet Sam. Sam is Government. Sam wants to borrow your money so his government can build hospitals, research weaponising viruses, build a bridge…whatever.

Lending money to Sam is pretty similar to lending money to Ben except Sam has the following tricks up his sleeve:

Governments pay their debts from the taxes raised on its citizens. If they need more money, they can raise taxes (the swine’s)

Governments also control their nations currency and have the option to magic money into existince using Quantitative Easing

Every insurance company, pension fund and most large institutions own government bonds. As governments have so many options to pay their debts a lot of them are considered ‘risk free’. This is a nonsense that we will explain in Part 2. It’s a lot of work trying to establish how safe a government (or company) is to lend to and fortunately an entire industry sprouted up to help with just that problem…

Bond Investment Terms

There will be different time scales for the debt and the name of the product will give you a hint of the time scales:

Notes - 2 to 5 years

Bonds - 10 years

Long Bonds - 30 years

Credit Risk

This is the risk a company/government is of defaulting and being unable to fulfil its contractual obligation of repaying the money it has borrowed. Credit Rating Agencies will typically provide a figure for this.

“When you are long credit you are short volatility” - Gregg Foss

Translation: Bonds with their fixed income and known returns should not be volatile, you know you have problems if prices on the sloppy seconds market (place to buy/sell bonds that havent matured yet) is swinging as that suggests the company/government is in trouble.

Conclusion

Before you buy debt from Ben and/or Sam (or on the sloppy seconds market) it would really help if someone did loads of research to tell you how likely you are to get your money back from them.

You can find the answer to that in Part 2

Here. <—— Click it 😘

Until Next Time

The Wealth Gap Team