The Debt Markets Saga! Part 2/3

Part 2 of the Debt Markets Saga

Welcome Back!

This section is Part 2 and you will be surprised to find that it follows on from Part 1.

In Part 1 we explained what debt instruments look like and what they do. In this section we look at the following:

Who gets to feast on the corpse of a company first when it goes into liquidation

The Credit Rating Agencies and its scoreboard

The Great Financial Crash and the Credit Agencies greatest failing

The Secondary Market

Who Gets to Feast First…

We mentioned in Part 1 that when a company goes into liquidation, the bond holders get first dibs on the company assets in order to salvage their investment. It won’t be a surprise to discover that not all bonds are created equal and that there are a myriad of terms, degrees of subordination and restrictive covenants in place to organise the pecking order. As the banking relationship is key for funding it won’t be a surprise to find the banks typically position themselves at the front of the queue whilst also getting the most generous returns (the sly dogs).

Credit Rating Agencies (Gaugers of Risk)

To help establish how risky a Bond is we can ask a Credit Rating Agency. These guys (S&P & Moodys) are paid by Bond Issuers to rate the safety of their offerings (HUGE conflict of interest).

Credit Rating Scores:

The Junk debt is where all the big gains can be made (higher risk higher reward). Remember that we are still talking about bonds and if a company gets liquidated the bond holders can try and claim their money back from the company’s assets (Share holders can’t). If a company’s bonds are Junk (big risk it can’t pay its debts) then its Shares should be really rubbish but a lot of professional managers won’t/can’t touch junk bonds (because they are junk) but will buy the Shares of that same company. This is a failure of money management ideology. An investment committee in a fund will have sat down and said ‘you can’t buy junk bonds without authorisation’ but won’t stop the fund manager buying the Shares.

The Great Financial Crash

The 2008 financial crash was caused by the subprime mortgage market collapsing. The subprime mortgage market was where Banks were building and selling big boxes of mortgages as products. The idea was each product would have a basket of mortgages ranging from safe to risky. The risky stuff offered a higher return so including them in the product boosted the income it generated. These were so popular that the banks ran out of safe mortgages to shovel in, meaning the products got more and more risky. Demand for mortgages got so high that anyone could get a mortgage and many people got multiple mortgages, all of which were piled into these products. Once everyone realised what they were buying were worthless the market crashed, tanking the world with it.

The credit rating agencies were left with egg on their face as they had been branding all these products as AAA/Aaa (super safe).

Anyway they are all still in business (🤢) and their ratings are still used to assess the quality of corporate and government bonds (🤮). When providing a rating they will factor in the below

The Secondary Market

There is a huge sloppy seconds market for bonds where prices fluctuate based on the winds of change. Prices are based on the bonds Yield to Maturity and the markets opinion on how likely those yields will be made. Lets bring Ben back at this point.

We lent Ben £100 in part 1 and he was contractually obliged to pay us £5 a year for 5 years + our original £100 back (£25 profit). In year 2 you hear Ben is going through a rough patch and you worry he might default and you wont get your money back. You can try and sell your Bond. It’s year 2 so you have had £10 from Ben already, you could sell your bond for £90 and have not lost any money.

Nobody will buy your Ben Bond for £90 (news of Ben’s bad news has travelled fast).

You panic and sell your Ben Bond for £80, thus making a £10 loss.

Scenario 1: The new owner holds the Ben Bond until maturity, picking up 3 payments of £5 on the way and collects original £100 back at maturity (£35 profit on their £80 investment). They took a risk and it paid off (jokes on you).

Scenario 2: Ben defaults in the 4th year after the new owner has received 2 payments of £5 (£10 total). As the bond allows the new owner dibs on Ben’s assets they are able to salvage £60 of the original. On their £80 investment they take away £70, losing £10 in the process.

Contagion

Contagion is the spread of one economic crisis from one market to another. Imagine if everyone in the world held lots of Ben Bonds and he suddenly tells everyone he might default. The secondary market would be inundated with people selling Ben Bonds. As there was so many Ben Bonds for sale the price tanks and everyone loses money. People might start selling more of their other investments because they are upset and want to protect their remaining funds. Now everyone is selling everything and prices are plummeting everywhere. Everyone is panicking.

Welcome to a Financial Crash.

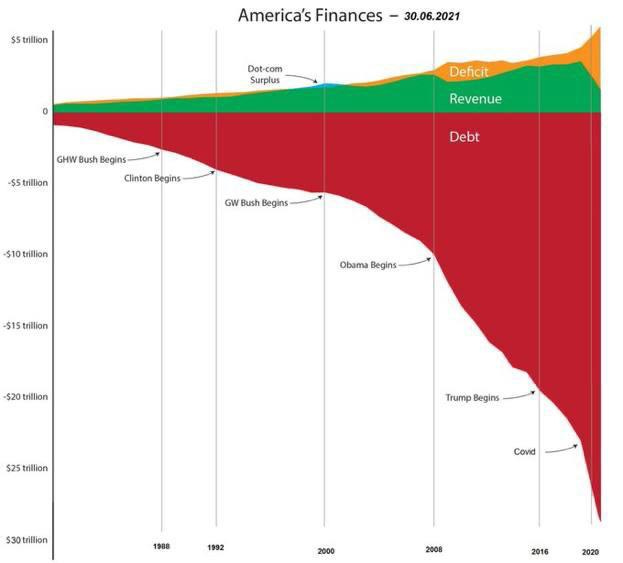

Remember Sam (Government)…?

Let’s imagine you lent Sam money. You agree to loan him £100 and Sam agrees to pay you £5 ever year for 5 years before finally returning the £100 (In 5 years you will get £125 back).

Sam can repay you but the game is his debts are WAY bigger than his income and its never going to get much better:

Sam has two tricks which keeps the game going:

Borrow more money to pay you off

Print the money and give you that

Sam decides to increase the number of £ in circulation by 30% (US government actually did this with dollars during the covid pandemic). Your annoyed with Sam because while he gave you your money back + profit its actually lost 30% of its purchasing value and your worse off overall. You would be even more annoyed if you had bought a 30 year bond from Sam and he was debasing the currency every year. Printing money stinks if your a bond holder.

Sam doesn’t give a shit though because he controls the currency that everything is priced in. Unfortunately for Sam he is annoying everyone and they might start pricing their stuff in currencies he can’t control.

So, what do you do now…?

You should come find out here

Part 3 <—— Don’t click this! 😋

The Wealth Gap Team